The Balanced Modernizer: Solid Everywhere, Exceptional Nowhere, And Why That's Dangerous

Financial Services / PageThere's a version of this profile that looks, on paper, like it should be the easiest to manage.

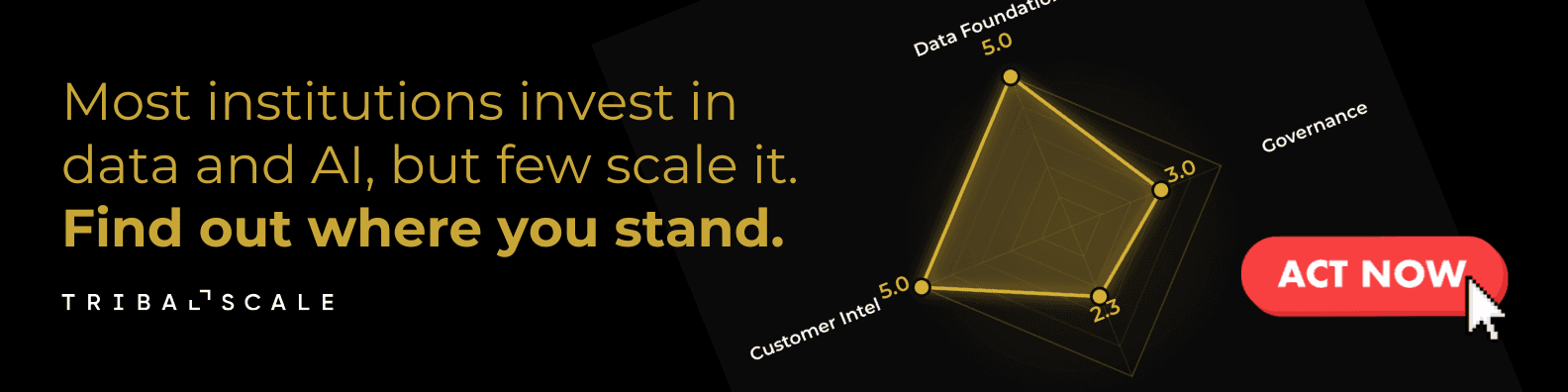

Data Foundation is at 3.2. Governance is at 3.5. AI & Real-Time Decisioning is at 3.0. Customer Intelligence is at 3.3. No critical gaps. No glaring weaknesses. Solid investment across all four pillars. The radar chart is nearly symmetrical — a shape that suggests consistency, thoughtful allocation, and steady progress.

The CEO looks at this profile and sees an institution that's doing things right. The board sees a balanced portfolio of technology investments. The CTO sees a team that's executing across multiple fronts.

And from the inside, it feels like everything is working. Which is exactly what makes this profile dangerous.

The Balanced Modernizer is the archetype where institutions get stuck — not because anything is broken, but because nothing is broken enough to force the kind of concentrated bet that separates good from exceptional.

The Pattern

On the TribalScale Financial Services Modernization Index™, the Balanced Modernizer scores in the 3.0–4.0 range across all four pillars, with a gap score (the difference between the highest and lowest pillar) of less than 1.0. There's no single pillar pulling ahead and no single pillar dragging behind.

The data foundation exists and functions. It's probably cloud-based or hybrid, with reasonable data quality and a working data catalog. Governance is in place — not fully automated, but defined and followed. AI capabilities are real but limited to a handful of use cases, mostly in pilot or early production. Customer intelligence has moved beyond basic segmentation but hasn't reached real-time personalization.

This is the "standardizing to integrated" transition zone — the range where most capabilities have been established but none have been fully scaled.

The Balanced Modernizer has done the work to leave the Legacy Operator stage behind, has avoided the imbalances that create the AI Experimenter or Compliance-Driven profiles, and has invested consistently. By most internal measures, the institution is performing well.

By competitive measures, it's in a holding pattern.

Why It Happens

Balanced investment was the strategy. Many institutions explicitly chose a "no pillar left behind" approach to modernization — and with good reason. The risks of over-investing in one pillar at the expense of others are real (the AI Experimenter and Infrastructure-First Institution are proof). The Balanced Modernizer's leadership made a conscious decision to advance on all fronts simultaneously. This was a risk-mitigation strategy, and it succeeded at mitigating risk. What it didn't do was create a breakout capability in any single dimension.

The organization rewards consistency over ambition. In most financial institutions, the performance management and budgeting systems reward steady progress and penalize volatility. A pillar team that delivers consistent 10% improvement year-over-year gets funded. A pillar team that proposes a concentrated 60% investment increase to leap from "standardizing" to "adaptive" gets questioned, scrutinized, and often scoped down. The organizational incentive structure pushes toward balanced allocation — which is how you end up with balanced results.

Nobody owns the "next level" conversation. The Balanced Modernizer's challenge is not technical — it's strategic. The question isn't "what's broken?" It's "what should we be exceptional at?" That question requires someone with the authority and vision to make a portfolio-level decision: we're going to disproportionately invest in one pillar because that's where competitive advantage lies for our institution in our market. In most Balanced Modernizers, this person either doesn't exist (the investment decisions are distributed across pillar owners) or doesn't have the political capital to redirect resources away from teams that are performing well.

The benchmarking trap. Balanced Modernizers love benchmarking — and benchmarking loves them back. When you score 3.0–3.5 across the board, you're above industry median on every dimension. The benchmarking report says you're "above average" and "well-positioned." This is accurate and unhelpful. Being above average across the board does not create competitive differentiation. It creates comfortable mediocrity. The institutions that are winning market share, capturing talent, and building moats are the ones that are in the 4.5+ range on at least one pillar — and they got there by making a concentrated bet, not a balanced one.

The Hidden Risk

The Balanced Modernizer's risk is the most psychological of any archetype. It's complacency masquerading as competence.

The plateau becomes permanent. The transition from "standardizing" (3.0) to "integrated" (4.0) to "adaptive" (5.0) is not linear. Moving from 1.0 to 3.0 requires investment and execution. Moving from 3.0 to 4.5 requires strategic focus, organizational transformation, and concentrated bets. The Balanced Modernizer can keep incrementally improving across all pillars indefinitely and never cross the threshold into genuinely differentiated capability. The 3.0–3.5 range is a local maximum — a point from which incremental improvement in all directions produces diminishing returns.

Competitors are making concentrated bets. While the Balanced Modernizer invests evenly, competitors are choosing a pillar and going deep. The institution that decides "we're going to be the best at real-time customer intelligence in our market" and concentrates investment accordingly will, within 18 months, have a capability that the Balanced Modernizer can't match without a similar concentrated effort. Multiply that by three or four competitors each making different concentrated bets, and the Balanced Modernizer finds itself above average everywhere and best-in-class nowhere.

The talent problem is different here. The Balanced Modernizer doesn't struggle to hire like the Legacy Operator. But it struggles to hire the best. Top-tier data scientists, AI engineers, and product managers want to work at institutions that are doing something exceptional — institutions where they can build at scale, push boundaries, and work on problems that don't exist anywhere else. An institution that's "solid across the board" is a reasonable employer. It's not an exciting one. The Balanced Modernizer attracts solid-but-not-exceptional talent, which reinforces the solid-but-not-exceptional trajectory.

The Highest-Leverage Move

The Balanced Modernizer needs to break symmetry. The single highest-leverage move is to pick one pillar and fund it to excellence — from 3.0–3.5 to 4.5+ — within three to four quarters.

This is a portfolio-level strategic decision, not a technology decision. It requires answering one question: Where does disproportionate investment create the largest competitive advantage for this specific institution in this specific market?

The answer depends on context, but the decision framework is consistent.

If your institution's competitive differentiation is customer experience — you compete on service quality, relationship depth, and retention — then Customer Intelligence & Personalization is the pillar to accelerate. Invest in real-time personalization, next-best-action engines across all channels, and hyper-personalized communication. Make your customer intelligence capability something competitors can't match without three years of catch-up.

If your institution's competitive differentiation is operational efficiency — you compete on cost structure, speed, and straight-through processing — then AI & Real-Time Decisioning is the pillar to accelerate. Invest in AI-driven underwriting, automated claims processing, real-time fraud detection, and intelligent routing. Make your decisioning speed and accuracy a structural cost advantage.

If your institution's competitive differentiation is trust and risk management — you serve regulated industries, high-net-worth clients, or institutional customers where governance and compliance are competitive differentiators — then Governance & Regulatory Readiness is the pillar to accelerate. Invest in automated compliance monitoring, real-time risk scoring, and governance-as-a-platform. Make your governance maturity a selling point, not just a cost center.

The pillar you don't choose doesn't get abandoned. It gets maintained at its current level. The teams keep executing their roadmaps. But the incremental budget — the investment that would have been spread evenly — gets concentrated on the acceleration pillar.

This feels uncomfortable for the Balanced Modernizer. It feels like creating an imbalance, which is the opposite of what got you here. But the transition from good to exceptional requires asymmetry. You can't be the best at everything simultaneously. You can be the best at one thing and strong at everything else — and that's a more defensible competitive position than being above average across the board.

What This Looks Like in Practice

Consider a Canadian wealth management firm — $45B in assets under management, serving both mass affluent and high-net-worth segments. Over five years of consistent technology investment, they'd built a solid foundation: cloud-based data platform, defined governance processes, two AI models in production (portfolio rebalancing alerts and client risk profiling), and segment-level personalization for client communications.

Their Modernization Index profile: Data Foundation at 3.4. Governance at 3.2. AI & Real-Time Decisioning at 3.0. Customer Intelligence at 3.3. A textbook Balanced Modernizer.

Internal reviews consistently rated the technology function as "on track." The firm benchmarked well against industry medians. The CTO's quarterly report showed progress on all fronts.

The wake-up call came from client attrition. The firm lost a cluster of high-net-worth clients — $2B in AUM — to a competitor that offered hyper-personalized, real-time portfolio insights delivered through a digital platform that made the firm's quarterly PDF reports feel like relics. Exit interviews revealed a pattern: the clients didn't leave because of performance. They left because the experience felt generic.

The CEO made a strategic decision: Customer Intelligence & Personalization would become the firm's breakout capability. The CTO was directed to reallocate 40% of the discretionary technology budget — roughly $8M — from balanced investment across all pillars to a concentrated customer intelligence acceleration program.

The program over three quarters: real-time portfolio insight engine (personalized to each client's holdings, goals, and risk profile), AI-driven life event detection (retirement planning triggers, liquidity events, estate planning moments), next-best-action for advisors (surfacing the single most relevant conversation topic before every client meeting), and personalized digital experience (moving from segment-level to individual-level communication across email, app, and advisor interactions).

The other three pillars continued their existing roadmaps. Data Foundation maintenance continued. Governance processes were unchanged. The two existing AI models kept running. Nothing regressed. But nothing in those pillars received incremental investment for the year.

Within 12 months, the firm's client retention rate improved measurably in the high-net-worth segment. More importantly, client acquisition in the mass affluent segment accelerated — the personalized digital experience became a competitive differentiator in a market where most competitors were still sending quarterly PDF reports. Advisors reported that the next-best-action tool transformed their client conversations from generic check-ins to targeted, relevant discussions.

The firm went from Balanced Modernizer to something closer to a Digital Leader in one pillar — while remaining solidly in the standardizing-to-integrated range on the other three. That asymmetry wasn't a weakness. It was the strategy.

Find Out Where You Stand

The Balanced Modernizer is the most comfortable profile in financial services — and comfort is the enemy of differentiation. If your institution is investing consistently, progressing on all fronts, and benchmarking above average, you may be in the most deceptively risky position of all.

The TribalScale Financial Services Modernization Index™ maps your institution across all four pillars in about five minutes. You'll see whether your profile is balanced — and whether balance is working for you or keeping you stuck.

This is Part 5 of our Six Profiles of Financial Services Modernization series. Next week: The Digital Leader — the institution that's built what most competitors are still planning, and why the game doesn't stop there.